If your credit is not as strong as you would like it to be, then you may be thinking about how to improve it. Sometimes, this leads people to professional credit repair agencies. As we have said before, using a credit repair agency is generally not worth it. That is not to say that they cannot provide value, but they are not able to do anything that you could not do yourself, and their services are not free or guaranteed. However, the same as debt settlement, credit repair comes in both the professional and do-it-yourself (DIY) varieties. The DIY approach is safer and more cost-effective.

With that in mind, let’s take a look at some techniques you can use to repair your credit without needing to hire an agency. We will also discuss some tactics to avoid.

Background

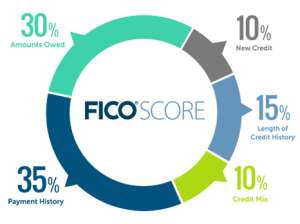

Before you attempt any credit repair, make sure you familiarize yourself with the credit landscape. As a reminder, what you think of as your “credit” essentially boils down to two components: your credit report and your credit score. Your credit score is determined by an algorithm that analyzes the information in your credit report. Therefore, you will be trying to improve the information contained in your credit report to improve your credit score. We have shared this image many times, but remember that these are the elements that are used in your credit score for the FICO scoring model:

Source: myFICO.com

Because your score is based on your report, your first step will be to review your credit report. If you are proactively trying to solve an existing credit problem, then it likely makes sense to pull your credit report from all three major reporting bureaus: TransUnion, Equifax, and Experian, since each one may have unique information. Alternatively, when you are just maintaining your credit standing, it may make sense to check your report from one bureau every 4 months, which you can do for free at annualcreditreport.com. Due to the pandemic, AnnualCreditReport.com has made it free to pull your credit report weekly from all three credit bureaus through April of 2021 so that consumers can stay on top of their credit reports and watch for any identity theft or fraud.

With your credit report in hand, you can begin working on the goal of making positive changes to the various credit score components.

Dispute Misinformation

If something on your credit report appears incorrect, then you have the right to dispute it and request to have it removed. The important point is that the information must be inaccurate—not just negative. You cannot unilaterally remove accurate but negative information from a credit report in a way that will be legitimate or permanent.

To dispute inaccurate information, you have a couple of options. The three major credit bureaus have developed online dispute systems. You can start a dispute at the following links:

That said, the FTC still recommends that you dispute via paper mail. This may have some advantages with creating a clear paper trail of your dispute. You can even use the FTC’s dispute letter template. Whichever way you choose to dispute, just make sure that you keep copies of any correspondence and that the bureau responds to your dispute in a timely fashion, within 30 days.

Submit Goodwill Letters

Sometimes the information hurting your credit score is accurate and negative. In that situation, you do not have a case to plead with the bureaus, because it is their job to report accurate information provided by creditors. Instead, you will probably have to wait for the negative information to fall off your report after the relevant amount of time has passed (usually seven years).

One option you could try, though, is asking the creditor for leniency. If it sounds like a longshot, that’s because it is a longshot! But it cannot hurt to try, and sometimes this strategy is successful. You can make this appeal to the creditor through a goodwill letter. In a goodwill letter, you directly ask a creditor to remove negative information from your credit report. You will have the best chance of success if you can provide a compelling reason for why you missed your payment(s) and/or can demonstrate that you have made consistent payments since your missed payment. NerdWallet has a helpful goodwill letter template.

Three Other Strategies to Try

Disputes and goodwill letters naturally fall under the “credit repair” umbrella because they are methods that can remove negative information from a credit report. However, another way to think of “repairing” your credit is to build it up moving forward, focusing on adding new positive information instead of removing negative information. Here are three basic strategies to consider implementing:

1) Keep accounts open if you can

Sometimes when you are working on your credit, it is tempting to close accounts. However, leaving accounts open will often improve your average account age, helping your score. There is a fine line here, though. If closing your account(s) will help you avoid putting extra, unaffordable charges on the account, then closing would likely outweigh the benefits of leaving them open.

2) Ask for higher credit limits

This can also be a bit counterintuitive, but having more credit available can improve your credit score. Simply asking creditors for a higher limit and receiving it should boost your score—all things being equal—if you do not increase your credit usage after receiving the increase. This method helps your credit utilization, which is a very important factor in your score.

Again, you have to be careful here. You need to ensure that having more credit available to you will not lead to increased spending and debt.

3) Meet your current and future obligations

This may sound like a no brainer, but that does not mean it isn’t important! One of the best cures for a credit score is simply to build a long-term trend of making on-time payments. You do this by working to ensure that your credit balances are manageable and by budgeting carefully. Ideally, you will work toward paying off your balances in full each month.

Depending on your existing debt load and your income, this may be relatively easy to do or it may be very difficult. Credit counseling can help you sort it out and make a plan for paying your debts for the long-term.

Strategies to Avoid

So far, we have discussed strategies that you can manage yourself and be successful. But there are a few tactics that you will want to avoid because they can do more harm than good. Here is a closer look at two of them.

Piggybacking

Piggybacking is the practice of being added to someone else’s credit account as an authorized user. Many times, the authorized user is added without being given actual access to the account (in other words, they are not given a credit card tied to the account). This strategy sometimes works, because the account is added to the credit report of the authorized user.

If the primary account holder uses the account effectively and without accruing negative marks, then these positive attributes can help the piggybacking party. However, if the primary account holder gets into financial difficulty on the account, then the piggybacking party’s credit score could take a hit. Another caveat: some creditors do not report authorized users to the credit bureaus, meaning that in those cases the piggybacking party would not see a benefit.

So while this can work, it is risky. It would be one thing to make this arrangement with a family member (note, that would still be risky), but it is entirely another thing to use a piggybacking company. Experian lays out multiple concerns about using a piggybacking agency, including legal implications, costs, and disfavor from lenders.

File Segregation

This tactic is typically encouraged by illegitimate credit repair agencies, though an individual consumer could pursue it. In either case, this is a very bad idea and definitely illegal.

File segregation involves creating a new taxpayer ID, usually an Employer Identification Number (EIN) and applying for credit under the EIN. By doing this, a consumer could trick creditors into granting credit, because the consumer’s individual credit history might be overlooked. The creditor essentially would not know that it was really working with an individual who had a poor credit profile.

Take the advice of the St. Louis Federal Reserve, and avoid this strategy at all costs, otherwise you will likely end up in deep legal trouble.

Moving Forward

Remember that professional credit repair typically does not offer enough bang for the buck. You are often better off disputing inaccurate negative information yourself. You can also try a goodwill letter to remove accurate but negative information. These are the primary legitimate credit repair strategies.

Moving forward, you should also try to keep a low credit utilization ratio, build up your average age of accounts, and be sure to make timely payments. Taking these steps will help you build a solid credit score that can remain strong for the long-term.

If you want more help reviewing your credit report or making a plan to stay on top of your financial commitments, you can get started with a credit counselor today.